Source :

Apple Intelligence :

• T-bill Yield Decline: Singapore Treasury Bills (T-bills) yields have declined from a peak of over 4% in 2023 to 2.12% currently, making them less attractive than CPF OA interest.

• Reinvestment Risk: Investors face reinvestment risk as maturing T-bills can no longer be rolled over into equally attractive investments.

• Inflation Impact: The current T-bill yield of 2.12% is below Singapore’s long-term average inflation rate of 2.59%, resulting in a loss of purchasing power.

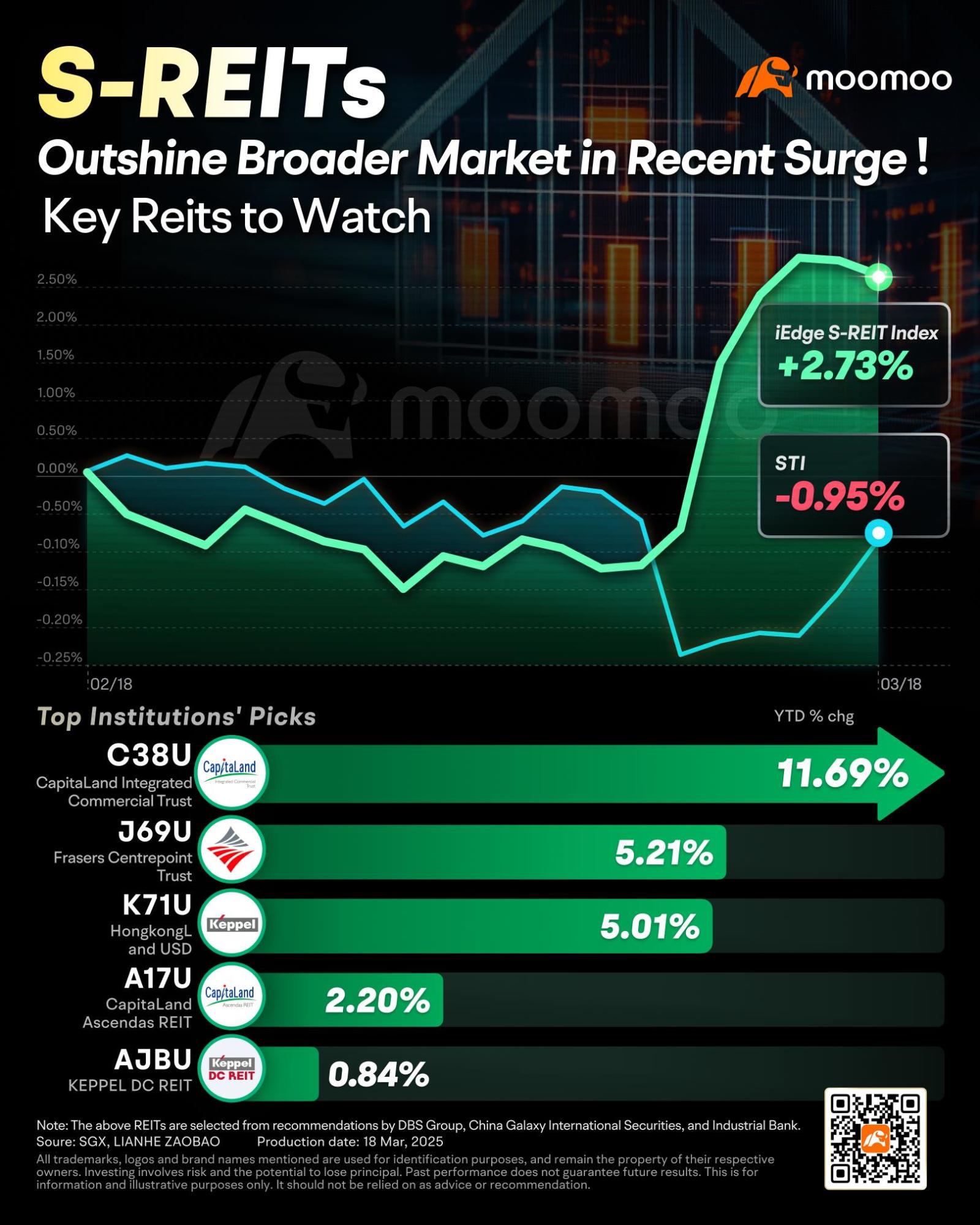

• Investment Alternative: REITs offer higher yields compared to T-bills, making them an attractive option for income-seeking investors.

• Yield Comparison: Singapore-listed REITs offer an average yield of 6.9%, significantly higher than the 2.12% yield of 1-year T-bills.

• Risk Considerations: REITs come with higher risk compared to T-bills, including price volatility and no capital guarantee, but these risks can be managed through diversification and a long-term perspective.

• Risk and Return: REITs offer a better risk-reward profile than regular stocks, with lower volatility and higher dividend yields.

• Investment Option: REIT ETFs provide diversification across multiple REITs, simplifying the investment process.

• Potential Opportunity: Falling REIT prices due to rising interest rates present attractive entry points for contrarian investors.

• Interest Rate Impact: Declining interest rates, as seen in Singapore’s SORA, benefit REITs by improving margins and potentially boosting capital gains.

• Investment Characteristics: REITs offer long-term income potential with dividends, avoiding reinvestment risk associated with fixed-maturity investments like T-bills.

• Liquidity and Flexibility: REITs provide greater liquidity and flexibility compared to T-bills, allowing for dollar-cost averaging and easy trading on exchanges.

• Investment Advantages: REITs offer ongoing income, flexible entry, and better liquidity compared to traditional real estate investments.

• Accessibility and Simplicity: REITs provide a straightforward and familiar investment option, especially for conservative investors, with business models centered around property ownership and rental income.

• Diversification and Tax Benefits: REITs offer diversification across a portfolio of properties without the high capital outlay of direct ownership, and they enjoy tax transparency, resulting in higher net yields for investors.

• Diversification Strategy: Diversify across income-generating assets like REITs and T-bills to build a resilient portfolio.

• Economic Environment and Asset Performance: REITs perform well during inflation and economic growth, while treasuries are favored during rising interest rates.

• Current Investment Recommendation: Rebalance portfolios by considering REITs, which offer higher yields (6.9%) compared to T-bills (2.12%), in the current low-interest-rate environment.