Source:

ChatGPT:

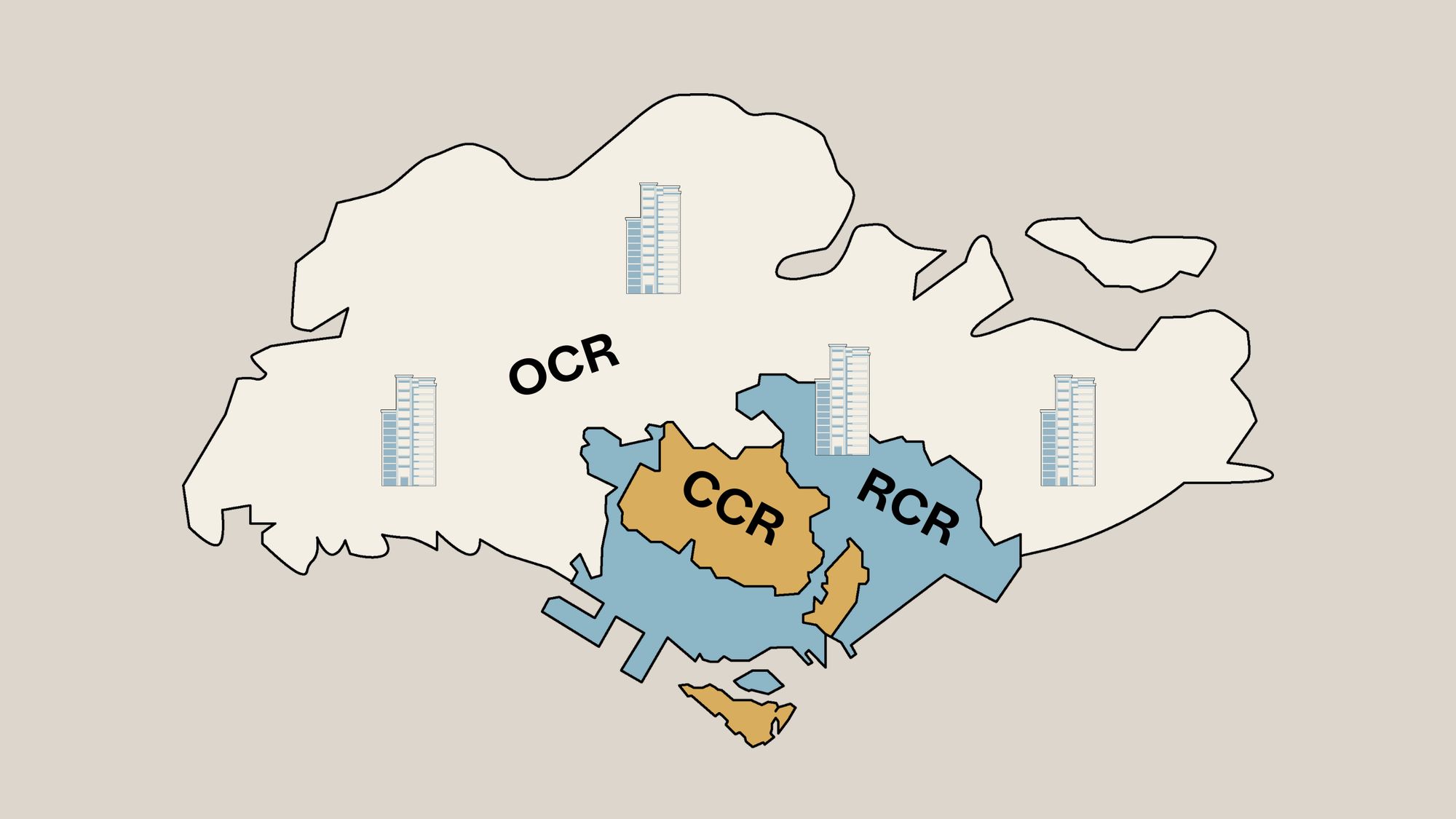

One major change is the pivot in new launches away from the Core Central Region (CCR) and back to the heartlands. While around 23 per cent of launches in 2025 were in the CCR, an estimated 65 per cent of 2026 launches will be in the Outside Central Region (OCR), including areas such as Tengah, Tampines and Bayshore. This matters not just for affordability, but also for liveability. OCR projects are more likely to offer family-sized three-bedroom units within the upgrader “sweet spot” of roughly $1.8 million to $2 million, something that was harder to find in CCR-heavy years.

Second, buyers face less urgency to purchase immediately. Private home completions are expected to rise from about 5,200 units in 2025 to around 7,000 units in 2026, as projects launched during the post-Covid boom reach completion. At the same time, new launches and overall new supply are set to fall. This combination eases supply pressure, encourages a more patient “wait-and-negotiate” mindset, and should help moderate price growth. It may also soften the rental market as more owners move into completed homes.

Third, the return of more executive condominium (EC) launches provides an important affordability bridge for buyers priced out of private homes. At least five ECs are expected in 2026, compared with just two in 2025, and demand is likely to be strong.

Finally, while interest rates have fallen to three-year lows, financing rules remain strict due to TDSR floor rates. Overall, 2026 points to a steadier, more rational market — a welcome change after years of excess excitement.

Comments:

Interesting insights.

No comments:

Post a Comment